Our history

SEK has helped the Swedish export industry with financing solutions for more than half a century. The Swedish government and the largest banks founded SEK in 1962, and the government became the sole owner in 2003.

Post-war times: New needs for financing

When Europe’s production apparatus was restored after World War II, competition intensified. Purchasers began to require more lavish credit conditions, a burdensome development for Swedish industry. The banking system wasn’t enough. The commercial banks wanted to start an export credit agency with state-supported guarantees.

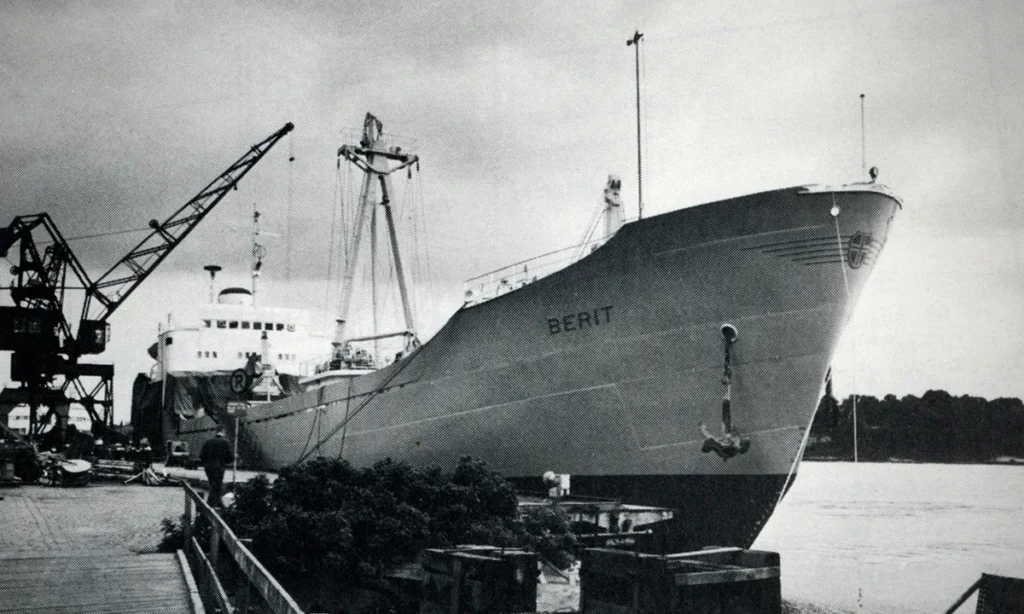

1962: SEK sees the light

When AB Svensk Exportkredit was founded in 1962, ownership was equally divided between the state and commercial banks. Our very first transaction was to finance the cargo vessel M/S Berit that was constructed at Finnboda shipyard between 1962 and 1963 for the purpose of exports to the Åland islands.

The 1960s and 1970s: Simplified lending

In the 1960s, SEK made a number of changes that simplified lending processes. More Swedish exporters received credit and thereby, strengthened their competitiveness.

The 1970s was a worrisome time. The oil crisis and the economic situation in OECD countries and developing countries alike generated new credit requirements. Most of the world’s credit providers were forced to offer more benefits to borrowers. This led to a number of international regulations in credit circles between 1976 and 1978.

The 1980s and 1990s: Strengthening our position

In 1978, the state-supported credit system (the SEK system) was introduced. SEK managed credit granting with subsidized interest rates and compensated for exchange rate losses. As a result, we were able to offer our clients the best conditions in Sweden. In 1979, we signed separate credit agreements with the USSR and China. To support Swedish exports, we provided state-supported export credits. In the 1980s, we developed new products that strengthened the Swedish export industry. At the end of the 1990s, the ABB replaced the banks as joint owner. The Swedish government has been the sole owner of SEK since 2003.

SEK today: Strengthening the export industry

Traditionally, our clients have been among Sweden’s many successful large companies, but some years ago, financing also became available for medium-sized companies with sales of at least Skr 200 million. We possess knowledge of the international capital market and understanding of the cultures and interests of different countries. SEK’s competence in international borrowing and lending is considered one of the best in the world today. We aim to use this knowledge and experience to help more Swedish companies to conduct successful business.